Home Mortgage Questions Answered In This Write-Up

Article written by-Lehmann McDanielWhat is the process for applying for a mortgage? Do you know anything about the terms or interest rates? This article can help you do just that, giving you the information you need to locate a good mortgage.

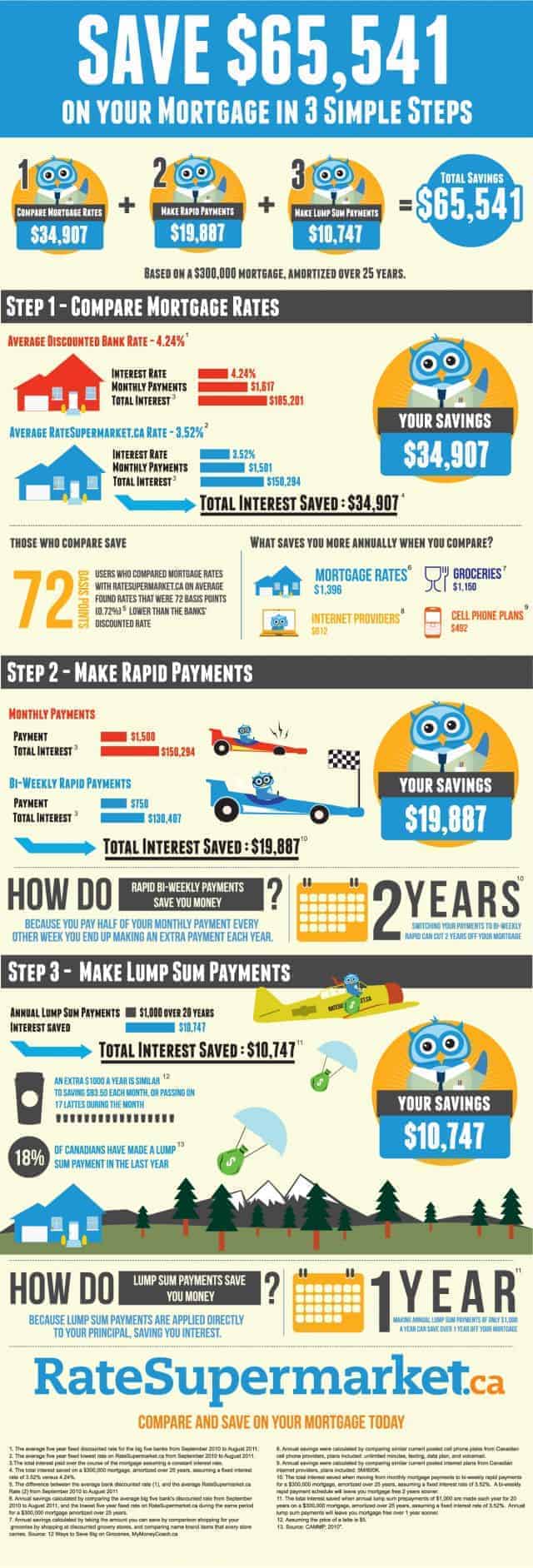

Have at least 20 percent of the purchase price saved. Lenders will want to verify that you have not borrowed the money, so it is important that you save the money and show deposits into your checking or savings account. Down payments cannot be borrowed; thus it is important to show a paper trail of deposits.

If your mortgage has been approved, avoid any moves that may change your credit rating. Your lender may run a second credit check before the closing and any suspicious activity may affect your interest rate. Don't close credit card accounts or take out any additional loans. Pay every bill on time.

It is likely that your mortgage lender will require a down payment. It's rare these days that qualifying for a mortgage does not require a down payment. Prior to applying for a loan, ask what the down payment amount will be.

Gather all your financial documents before seeing a mortgage lender. Your lender is going to require income statements, bank records and documentation of all financial assets. Being prepared well in advance will speed up the application process.

A solid work history is helpful. Many lenders insist that you show them two work years that are steady in order to approve your loan. Multiple job changes can also cause disqualification. You never want to quit your job during the loan application process.

It is better to have low account balances on several revolving accounts, rather than one large balance on a single account. If possible, keep all your balances under half of the limit on your credit. It is best if your balances total thirty percent or under.

It is better to have low account balances on several revolving accounts, rather than one large balance on a single account. Your balances should be less than 50 percent of the credit limit on a credit card. Keeping your balances under 30% of your credit limit is even better.

If you are offered a loan with a low rate, lock in the rate. Your loan may take 30 to 60 days to approve. If https://sanatogapost.com/2021/12/15/citadel-names-sutliff-business-head/ lock in the rate, that will guarantee that the rate you end up with is at least that low. Then you would not end up with a higher rate at the end.

If you are able to pay more for your monthly payments, it is a good idea to get a shorter-term loan. Most lenders will give you a lower rate if you opt to pay your mortgage over 20 years instead of 30 years. Borrowers who get shorter term loans (such as 15 or 20 years terms) are considered less risky than those with longer term loans, resulting in lower interest rates.

Pay off or lower the amount owed on your credit cards before applying for a home mortgage. Although your credit card balances do not have to be zero, you should have no more than 50 percent of the available credit charged on each credit card. This shows lenders that you are a wise credit user.

Be honest when it comes to reporting your financials to a potential lender. Chances are the truth will come out during their vetting process anyway, so it's not worth wasting the time. And if your mortgage does go through anyway, you'll be stuck with a home you really can't afford. It's a lose/lose either way.

Know the risk involved with mortgage brokers. Many mortgage brokers are up-front with their fees and costs. Some other brokers are not so transparent. They will add costs onto your loan to compensate themselves for their involvement. This can quickly add up to an expense you did not see coming.

There are times when the seller of a home will be able to give you a land contract so you can purchase the home. The seller needs to own the home outright, or owe very little on it for this to work. A land contract may need to be paid within a few years.

If you what to buy a house in the next 12 months, stay in good standing with the bank. Start by taking out a loan for something small before you apply for a mortgage. This will make sure your account is in good standing before you ever apply for a mortgage.

Don't be afraid of waiting for a better offer. Certain times will give you better deals than others. You may locate an option that works well since a new company is having a deal or the government has passed something new. Sometimes just waiting for the right time can really be the best decision to make.

If your mortgage lender will give you a letter of approval, it may open some doors with sellers. This type of letter speaks well of your financial standing. However, make sure that the approval letter is for the amount of your offer. If it shows a higher amount, then the seller will see this and realize you could pay more.

The posted rates at a bank are a guideline, not a hard and fast rule. Look for a competitor that has a lower rate. Let your lender know you plan on going to the lower rate and they may offer you that low rate.

During the process of obtaining a mortgage loan, submit any requested documents to your mortgage broker or lender as soon as possible. Taking your time to respond to your lender can delay the date of the closing. Delaying the closing date can put you at risk of losing the rate you have locked-in.

When you want to buy a new home, you'll have to find a mortgage you can afford. If your plan is refinancing or paying for renovations, you'll need to locate a mortgage which permits these uses. All of the tips in this article will help in either situation, so be sure to use them.